Property sales are 40% down from a year ago, and days on market (DOM) is up 13 days. Property prices have fallen 9.5% from their peak in November 2021 and the number of listings is up by 104%.

This profound weakness in the residential property sector has not come about because of a wave of distressed sellers. There is no evidence of a wave of investors selling ever since the tax rules were changed last year. The dummy was spit but no further action was taken.

Very few owners will end up paying a higher interest rate on their mortgage than they had to prove to the bank they could handle when they signed up for their purchase and debt 1, 2, 3 etc years in the past. The labour market is also exceptionally tight. Property owners are confident that if they’re laid off, they can easily get another job to help service their mortgage.

So, why has the housing market slowed down and gone into reverse?

Because the buyers have slipped back into the shadows. Why are they hiding out of sight? Because getting credit suddenly became a lot harder late last year. Mortgage interest rose 3%+ over a very short period of time. There was a cost of living crunch, and fears of prices rising and rising disappaited.

When will the buyers return and start soaking up the growing stock of listings?

To answer that it pays to have insight into the things which concern buyers most of all at the moment. That is information I can get from the monthly survey of residential real estate agents nationwide.

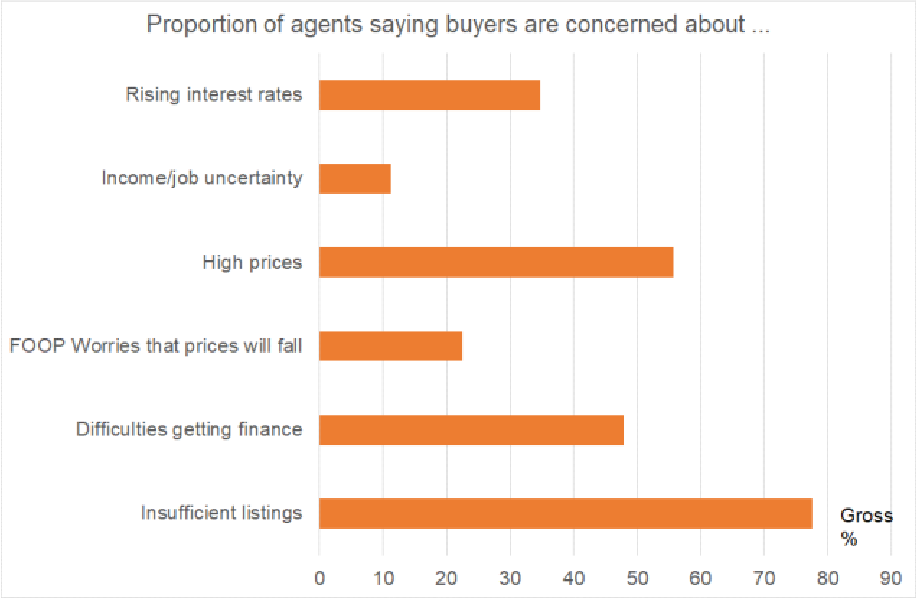

The following graph shows the proportion of agents in September 2021 who said buyers were worried about each variable.

- 35% were worried about rising interest rates.

- 22% said buyers were fearful of prices falling after they purchased.

- 78% said they were concerned about insufficient listings.

- 56% said high prices.

- 48% cited difficulties getting finance.

This is the situation now.

- 82% are worried about high interest rates.

- 78% cite worries about getting finance.

- 69% cite worries of prices falling.

- 11% say listings are a worry.

- 11% say employment is a concern, unchanged from September.

So, the big concerns are interest rates, financing, and price declines. The first two areas are improving. The last will follow before the end of the year and could even be changing now.

Interest Rates

Fixed mortgage interest rates have started to decline. This may not receive much attention in the media for some time because the focus will be on the cash flow implications of rate changes for those who fixed at low rates last year and are now rolling into something higher. But those people are not hesitant home buyers. They already have a house and a mortgage. Their spending plan changes have almost no relevance for the residential property market. Instead, it’s the buyers in the shadows that are relevant here. Over time, they’ll realise that we’ve already seen the peaks for almost all fixed lending rates for home buyers.

The Reserve Bank is set to take the official cash rate from 2.5% to a probable peak of 3.5%.

But fixed rates reflect market expectations of monetary policy and not where the cash rate sits at the moment. Those market expectations are for monetary policy to be easing by the end of 2023 with cuts continuing through 2024. Hence big falls in bank wholesale borrowing costs recently and the partial pass-through into their fixed lending rates.

These rate cut expectations reflect early signs of inflationary pressures easing off and worries about recessions in the likes of the United States and Europe increasing recently. International oil prices are down along with prices for minerals and food. Shipping costs are easing and supply chains functioning slightly better. A measure of online consumer prices in the US is now falling, the pace of rents growth here in New Zealand is easing, consumer inflation expectations have fallen in the ANZ’s monthly gauge, and the Reserve Bank’s Survey of Expectations held amongst market analysts has also just eased marginally. High inflation numbers will be with us well into 2023. But the direction of change outside countries which allowed themselves to become dependent on Russian gas is turning downward.

Over the next few months, buyer concerns about interest rates are going to fall away.

Access to finance

As noted last week, various gauges from my monthly surveys tell us that the credit crunch was at its worst very early this year.

Competition between banks for mortgage business is strong, and for the moment they are fighting that competition with cashback offers. Eventually, they will back away from such costly incentives and revert to discounted lending rates plus greater willingness to lend generally. Beyond that, there is a good chance that when house prices have gone down another 5.5% and the Reserve Bank then considers them to be

“sustainable”, that there will be an easing of LVR regulations.

Credit availability is likely to improve bit by bit for home buyers from here on out.

Worries about falling property prices

It will take some time for these concerns to fall away. But as each month passes and average prices go lower, more and more potential buyers will give thought to how close we might be to prices bottoming out and how much prices have pulled back from their ridiculous heights of late last year.

At some point buyers generally will lose their price fall fears, or just ignore them in the interests of securing a property from the large number of listings.

The measure of price decline worries which I derive from my monthly survey of residential real estate agents has in fact eased for two months in a row now. But the decline from 73% to 69% is very small and not enough for me to yet feel confident saying that we have passed peak FOOP – fear of over-paying.

The challenge to first home buyers

One interesting thing to consider is that in the coming weeks we may see first home buyers increasingly challenged to give thought to what matters to them. Do they hold off from buying because they want to avoid the last 5% fall in prices and buy at the bottom so they can feel clever? Or do they want a house in which to raise a family?

Last year they scrambled to find anything (unsuccessfully) when the stock of property listings was at a record low below 14,000. Now, listings are double what they were a year ago, and it is a buyer’s market in which home hunters can increasingly pick and choose.

Why would you not look to buy now when;

- Property prices are down 10%, (a lot more in some locations).

- Vendors are increasingly open to offers,

- Banks are increasingly eager to lend and may trade cash backs for discounted fixed rates,

- There are twice as many properties to choose amongst than last year,

- You have a job and can probably shift voluntarily to another one for higher wages,

- There is a greater chance of finding a property which meets your anticipated needs than at any other time since 2015,

- Migrants have yet to return in numbers.

- Investor buyers are sitting back waiting to see what happens with the election and not competing against current active buyers.

Also, keep in mind that construction costs are only going to keep going up.

The three main factors causing concern for buyers and making them stay back in the shadows will ease as we head into Christmas. All that is really in doubt is the speed of the easing and the lag in months between the buyers coming out of the shadows and average house prices moving back up slightly again over 2023.