Independent economist, Tony Alexander, provides an update on the housing cycle and discusses where it is likely heading.

New Zealand’s housing market is weak and getting weaker.

The number of sales in June was down 38% from a year earlier. The average number of days taken to sell a dwelling was 13 longer than a year before. The stock of properties listed for sale at the end of the month was 104% higher than a year ago.

House prices so far have fallen by 9.5% from their November nationwide peak and they probably have further to go. The results from my various surveys all show that we should expect weakness to continue over the next few months. For instance, we see that a record net 4.5% of people are planning to pull back on plans for buying a house to live in.

From my monthly survey, 7% of mortgage advisors say they’re seeing fewer first home buyers looking for advice. A net 44% are also saying they’re recieving fewer enquiries from investors. Furthermore, 47% of surveyed real estate agents report a decline in the number of open home attendees.

All in all, New Zealand’s housing market is looking grim, especially in the context of;

- near record low levels of business and consumer confidence,

- above average mortgage rates,

- the biggest hike in the cost of living since 1990, net migration outflows,

- collapsing developers, and,

- a soon-to-start collapse in the number of consents being issued for new dwellings to be built.

But what if we looked at the market from a different perspective? What if instead of saying what is the outlook, we were to ask this.

When will the buyers return?

My view is that buyers will start coming out of the shadows before the end of the year. We’ll see sufficient numbers of buyers re-engaging with the housing market through 2023. This will produce price rises averaging maybe 5%+, rising sales, and an eventual pullback in the stock of listings.

How can I justify a seemingly positive view when things currently point in the other direction?

A key driver is the state of the labour market.

Job opportunities abound, people know that if they get laid off they’ll be able to find another job quite quickly. That means very few people will be fearful of not being able to service their mortgage.

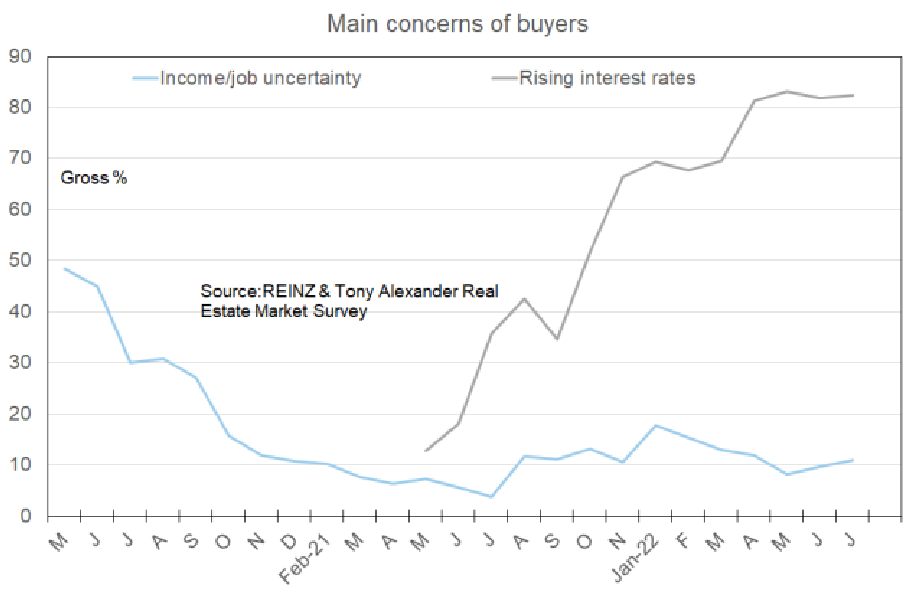

The buyers are still there – but in the shadows. One gauge of labour market strength can be garnered from my monthly survey of real estate agents with REINZ. This graph says a lot. It shows two of the factors which agents can report that buyers are worried about.

Shown as the light blue line we see no upward trend in observations that people are worried about their jobs. The grey line demonstrates a significant increase in the number of people worried about high interest rates.

An important figure because it increasingly looks like fixed mortgage rates have peaked for all but the one-year term. The cost to banks of borrowing money to lend fixed for periods of 2-5 years has fallen 0.5% – 0.8% since mid-June. Bank margins for three year lending are now almost above average. Scope may soon exist for cuts as we saw one month back for the two-year fixed term.

Central banks currently are raising their cash rates rapidly. Not so much to crunch their economies because they are already being slammed by a cost of living crisis. As noted previosuly, a 7.3% hike in the cost of living in New Zealand hits 100% of households. Rising mortgage rates affect only one-third, and for many of them, the dollars involved will be small.

Monetary policy is not as effective as a large cost of living hit in restraining consumer spending. Central banks are raising interest rates but will start adjusting these to better reflect the prospects for inflations once they reestablish credibility.

The financial markets are pricing in at least two rate cuts in the United States before the end of 2023. That is the sort of thing which heavily influences fixed interest rates in New Zealand for two years and beyond. The upshot is this. At some point, probably before the end of the year, worries about rising interest rates will fall. When that happens, buyers will likely step forward and more actively peruse the rising stock of listings.

But reduced interest rate fears won’t be enough. We will also need vendor capitulation. Where those sellers give up hope of achieving a price remotely close to what they could have got last year. They want to get on with their lives so decide to meet the market. We’re seeing tendrils of this currently, but nothing substantive enough to say we’re fully in the endgame for this period of house price declines. But we are getting close.

Interest rate predictions and vendor behaviour aside, there are other signs of the housing cycle getting set to turn within the next 6-9 months.

The extent to whcih real estate agents are reporting worsening numbers at open homes is easing.

This does not mean that more people are showing up. It means the deterioration is slowing. It is akin to falling in the water. You’ve hit the bottom, and are rising to the surface (you’re still drowning). Sometime after that you’ll be breaking through into the air.

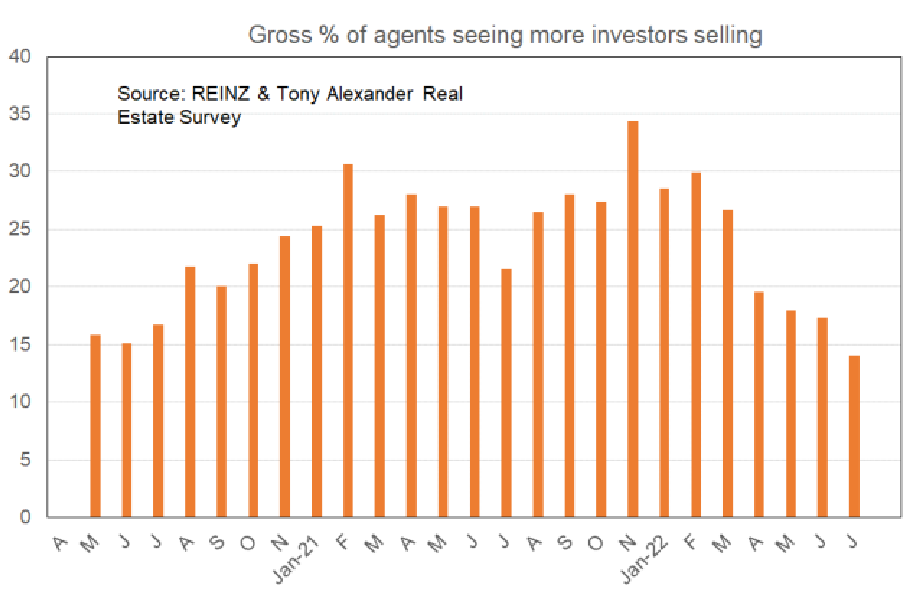

We’re seeing a decrease in the number of agents reporting seeing investors selling. To repeat my comment from April last year. There is no wave of investors selling.

And is it that FOOP is turning?

Then we get some interesting results of mortgage advisors almost reporting more first home buyers looking for advice.

Credit crunch easing

Another factor contributing to my view of the housing cycle is the easing of the credit crunch. We’re probably never returning to the accessibility of home buying credit that existed in the decades before alterations to the CCCFA (effective from December 2021). But the degree of credit tightness is on an easing path.

Mortgage advisers report that lenders are perceived as becoming more willing to advance funds. Residential property investors report reduced degrees of difficulty getting finance. We further see the shift in the credit crunch in data gathered by the Reserve Bank showing the proportion of new bank lending to borrowers with less than a 20% deposit. The proportion hit a low of just 5.1% in March but isnow back at 7.8%.

As yet there is no slam dunk case for saying things are improving. Or that they will definitely improve by some particular timeframe. No-one can deliver that level of accuracy.

And as yet, I am unwilling to coin the wording I used from some 15 or so months ago – namely that we back then had entered the endgame for the prices boom. But the tendrils are indicating things becoming less bad underneath the headlines of prices falling. Prices have further to go down, but the endgame for this period of price decline is approaching. I suspect when the turn comes, it will be quite sudden because of this economic cycle’s unique labour market strength.

The buyers have not gone. They have simply taken two or three steps back from the line into the shadows.

They will-re-emerge in numbers down the track. My best guess? Housing market reports heading into Christmas will be of a quite different tone to those you are reading now.

And what does this imply for house prices in 2023?

They will rise between 5% and 10% because 80% of what’s happening in the real estate market at the moment is not a structural shift. The absence of a flood of vendors tells us that once the huddled, job safe, buyers return, listings will quickly decline again, FOMO will return, and prices will climb anew, but not like they did before. Why? Because of higher average interest rates and structural reduced credit availability.

Oh, and one final thing to keep in mind regarding prices. Market prices are going down, but construction costs are going up. A natural level of support for prices is being created and is probably not far from where the market is now.

And finally, consider this quirk.

Once average house prices have fallen by another 5.5% to sit 15% down from their November 2021 peak, according to the Reserve Bank house prices in New Zealand will no longer be unsustainable and representing a threat to the financial system. We will be able to run a headline reading this “Reserve Bank feels house prices are now sustainable”. We are 5.5% away from official endorsement of NZ house prices.