New Zealand’s economy shrank by 0.6% during the December quarter. All the talk is that we may be already in recession or well on the way to one.

Let’s have some perspective.

First, the 0.6% shrinkage followed 1.7% growth in the September quarter and 1.6% growth in the June quarter.

If someone said “I’ll take $6,000 off you nine months from now. But before then I’ll pay you $16,000 and then $17,000.” I’d say sign me up.

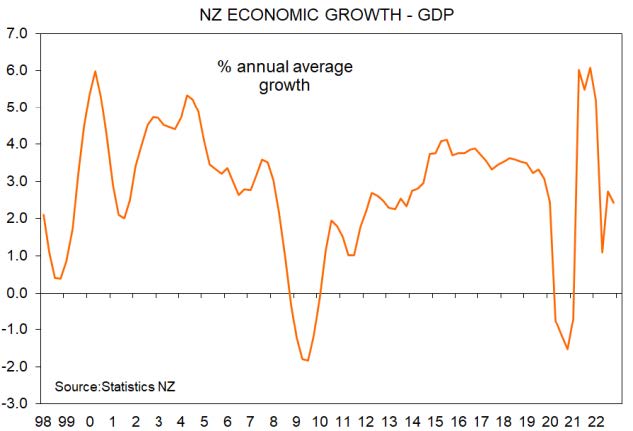

The economy is still 2.2% bigger than a year earlier. 6.6% bigger than before the pandemic. The growth rate this past year all up of 2.4% was only just below the average since 1989 of 2.7%.

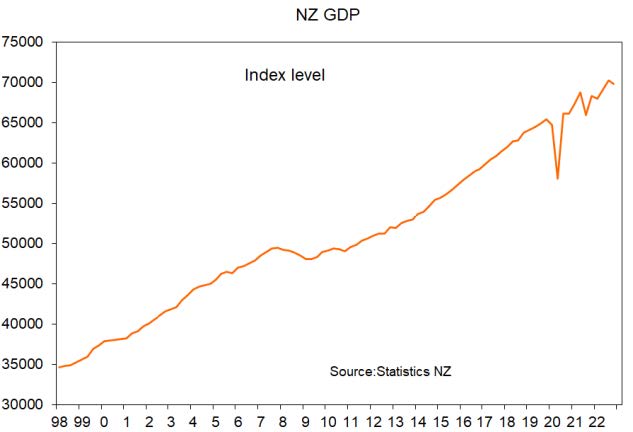

This first graph shows the annual rate of growth in our economy since 1998. This next shows the size of our economy in volume terms. The trend is decidedly upward.

Second, just because there’s woe around does not mean that a recession is in fact underway.

The data has been highly volatile on a quarterly basis for some time now. We could easily get a blip up for the latest quarter, or a blip down. Work associated with flood recovery will be a boost to economic activity.

Staff shortages

Third, part of the reason for the 0.6% shrinkage is that businesses didn’t have enough staff to produce demanded output.

We are trained to think of economic shrinkage as the result of not enough people and businesses here and offshore buying the things we make. But we have become a capacity-constrained economy in which demand cannot be satisfied because of a shortage of people.

The NZIER’s most recent Quarterly Survey of Business Opinion showed that still near record proportions of businesses say they cannot get the skilled and unskilled staff they need to boost output.

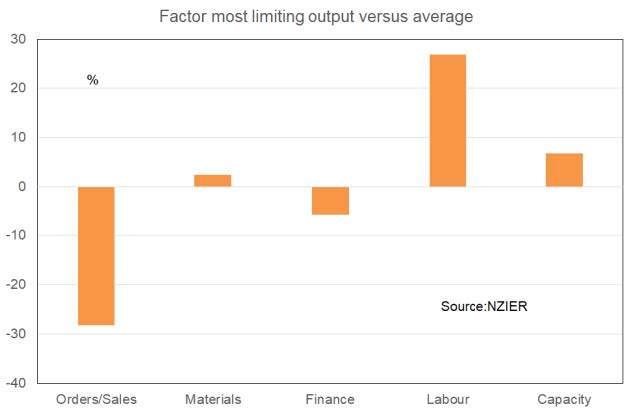

This situation can also be seen in response to the question of what factor is most constraining the ability of businesses to grow. On average since 1970 61% of companies have said demand. That now stands at only 33% and the difference is shown by the first orange column in the following graph sitting below the zero line.

Materials are only slightly rated above average as a constraint 7% versus average 5%) and the same for finance (2% versus average 5%). Bank credit is considered not really an issue by businesses.

Labour on average is cited by 11% of businesses as their main constraint. The latest reading is 38% and hence the orange column at high levels to the right side.

In a capacity-constrained economy, we cannot consider the absence of growth to be outright negative.

Traditionally this has been the case in New Zealand when a shortage of demand has been the issue. Many still worry when we hear the word recession because of the expected impact on the labour market.

When people hear the word “recession” they see a black-and-white photo in their heads of men queuing for work or assistance in the Great Depression.

But New Zealand’s unemployment rate is at a near-record low of 3.4%. People can pick and choose where they want to work. Businesses in the CBDs are forced to accept employee demands to work from home.

A recession these days is not the same thing as a recession before our labour market got structurally very tight from just before the 2008-09 GFC.

Post-recession changes

Fourth, how much woe really stems from a recession? Let’s see.

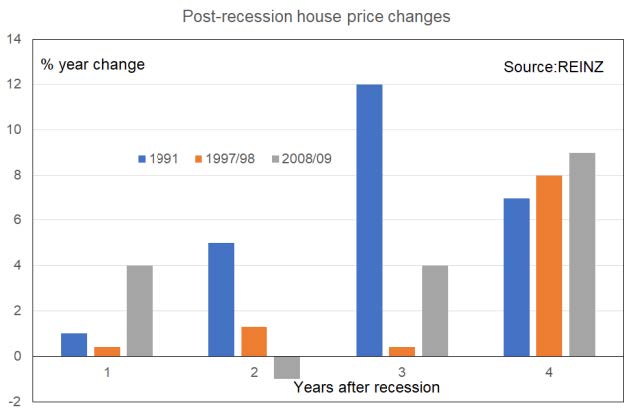

There was a recession in the first half of 1991 where the economy shrank by 3.1%. A year after average house prices rose 1%, then 5% then 12% then 7% come mid-1995. There was a recession from mid-1997 to early-1998 where the economy shrank 0.9% – the Asian Financial Crisis. A year later come early-1999 average house prices rose 0.4% then 1.3% then fell 0.4% then rose 8%.

The next recession was the GFC where the economy shrank about 3% over all of 2008 and the March quarter of 2009. Come early-2010 average house prices rose 4% then fell 1%, rose 4%, then rose 9%.

This graph shows annual house price changes in the four years following each of the three recessions.

There’s no consistent pattern of house price movements following a recession and the depth of the recession provides no guide. But rises occur more often than flatness or falls. Therefore, if we are in recession there is no way of telling what exactly this will mean for house prices. Other factors are relevant and that is where things differ and the house price bias moves to the upside.

At the start of the 1991 recession…

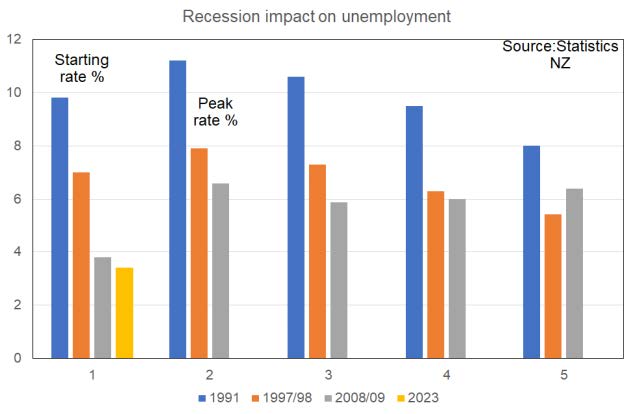

The unemployment rate was 9.8%. It rose quickly to 11.2%, and a year after the recession ended it was 10.6% then 9.5% then 8%.

At the start of the 1997/98 recession…

The unemployment rate was 7%. It peaked at 7.9% and a year after the recession ended was 7.3% then 6.3% then 5.4%.

At the start of the 2008-09 recession…

The unemployment rate was 3.8%. It rose to 6.6% and come early-2010 was 5.9%. A year later, 6%. Then 6.4%. Then 5.8%.

If we are in recession then the starting point for the unemployment rate was 3.4% – a record low.

This next graph shows as the first group of columns the unemployment rate heading into a recession. The next group shows the peak unemployment rate. The other three groups show the rate one, two then three years after the recession ended.

Will the unemployment rate now rise between 1% – 3% and if so how much?

Ahead of and through the 1991 recession virtually no businesses considered labour as an output constraint. Staff were easy to find. This meant little labour hoarding would have been undertaken. Ahead of the 1997/1998 recession, only 4% of businesses considered labour a constraint. On top of this, minimal difficulties finding people were being expressed. Again, the incentive to hoard staff was very small. Ahead of the GFC, an above-average 21% of businesses were finding labour to be an output constraint. A net 36% found skilled labour hard to find and a net 25% found unskilled people difficult to get.

Bank wobbles matter

Things were tight yet the labour market received a strong shock. That is what 3% shrinkage and deep fears of a new Great Depression will do. The GFC was a serious event which happened after we were already in recession. This was due to high mortgage rates from 9% – 11%. That is why everyone is taking the current bout of bank wobbliness very seriously. Banking sector troubles matter deeply.

Now, a near record 38% of businesses say labour is their main output constraint. A net 68% can’t get skilled people and 64% can’t get unskilled. We are not in a GFC event and mortgage rates have already peaked.

The extent to which the unemployment rate rises this time will be very small. The chance we reach the near 6% levels predicted by both Treasury and the Reserve Bank is virtually zero. Businesses are going to hoard staff to the best of their cash-flow abilities.

Only a mild period of labour market restraint with the unemployment rate likely rising to just over 4%, will prove a little problem for the housing market. Plus, price gains rather than flatness look likely once this recession ends – if we are in one.

Out-of-date and unreliable

Fifth, in truth, while GDP data is useful for comparing economies and measuring long-term economic development, they’re too out-of-date to be of much use to us economists.

They are distorted by pandemic effects we don’t fully understand. They also tend to get heavily revised as the quarters and years go by. Periods which technically were recessions eventually become not so and vice versa.

Throw in the capacity shortages in our economy and there is really no point in using the GDP data at all other than to try and get a feel for the degree of that capacity constraint. But such constraint is better estimated by looking directly at capacity measures. Such as in the Household Labour Force Survey and the NZIER’s quarterly report.

Other data sources are far more up-to-date and useful. Allowing us to gauge where we are right now and where we appear to be headed. Ignore them and take your own personal gauge by considering how many layoffs you see around you. Note, however, in some sectors layoffs represent payback after pandemic excess such as in tech.

If I were a borrower, what would I do?

Wholesale interest rates have fallen in New Zealand this week. The one-year swap rate of 5.22% from 5.32% last week is the lowest since the second week of January. Banks’ three-year cost of borrowing money to lend at a fixed rate is now near 4.63% from 4.75% last week.

I discuss the factors behind these developments in more detail in Tview Premium. Suffice to say, the driving forces lie offshore and domestically inflation remains a concern. So, we should still expect another 0.25% official cash rate increase to come in the next review on April 5. But, with regard to bank fixed mortgage rates, the track from here will be downward. However, at a very slow pace. Not anything like the sharp falls which occurred after the 1997/98 Asian Financial Crisis and the 2008/09 Global Financial Crisis.